- The Net Worth Club

- Posts

- 4 Resource Stocks Heating Up Right Now

4 Resource Stocks Heating Up Right Now

Momentum is building, and fast! (TGC, AUX, GLAD, MSA)

Danny Brody

October 02, 2025

Forwarded this newsletter? Subscribe Now! (It’s Free) 🚀

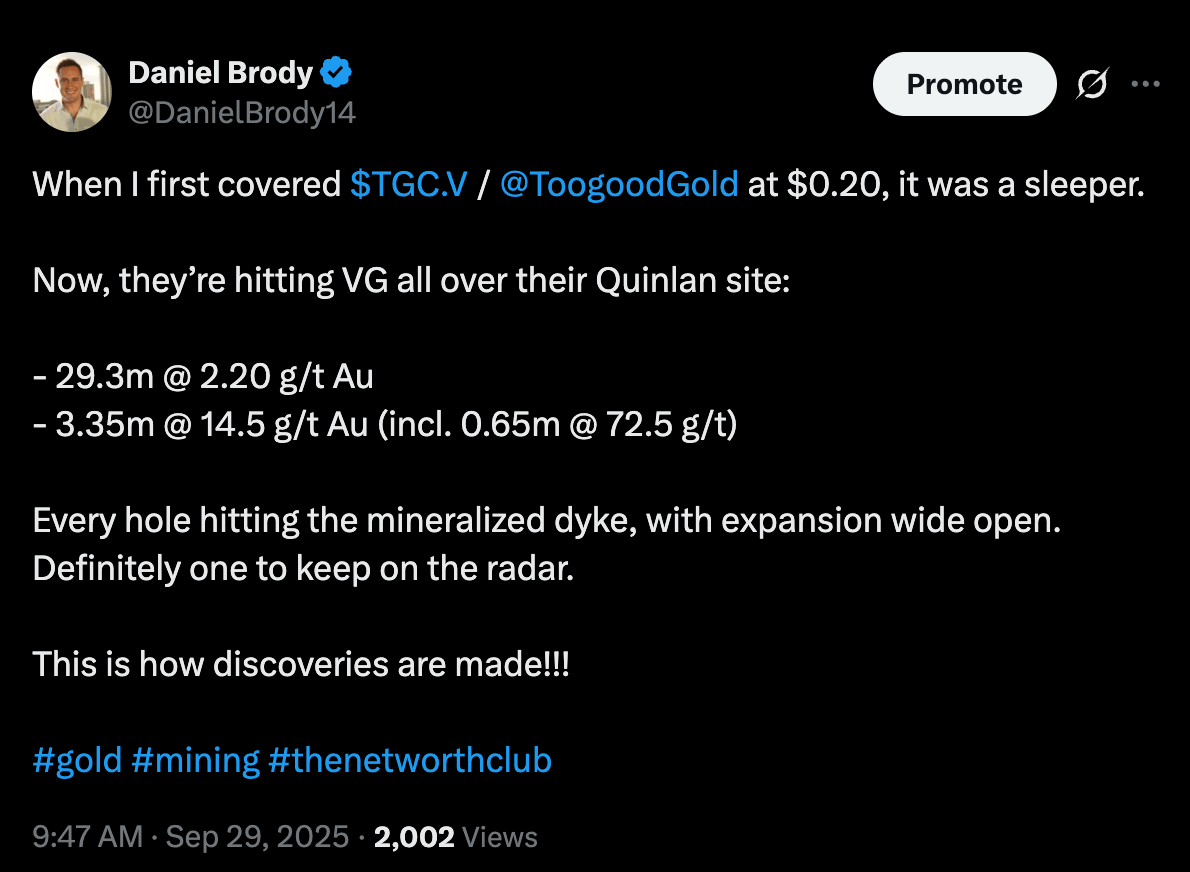

When I first covered TooGood Gold (TSX-V:TGC) at $0.20, it was a sleeper.

Follow me on X

And as noted here, they’re now hitting VG all over the place.

Every hole has hit the mineralized dyke they were shooting for.

A 100% hit rate.

With multiple near-surface, high-grade drilling intercepts including:

29.31 m @ 2.20 g/t Au from 35.00 m, incl. 0.99 m @ 11.42 g/t Au from 57.01 m;

3.35 m @ 14.48 g/t Au from 77.25 m, incl. 0.65 m @ 72.53 g/t Au from 77.25 m;

And visible gold (VG) has been identified in 10 of 30 drill holes logged to date in 2025.

Their high-resolution ground-penetrating radar ("GPR") survey even suggests possible untested geological continuity of their Quinlan site to north-northeast.

And, they’ve just gone public, in July.

All this in two months…

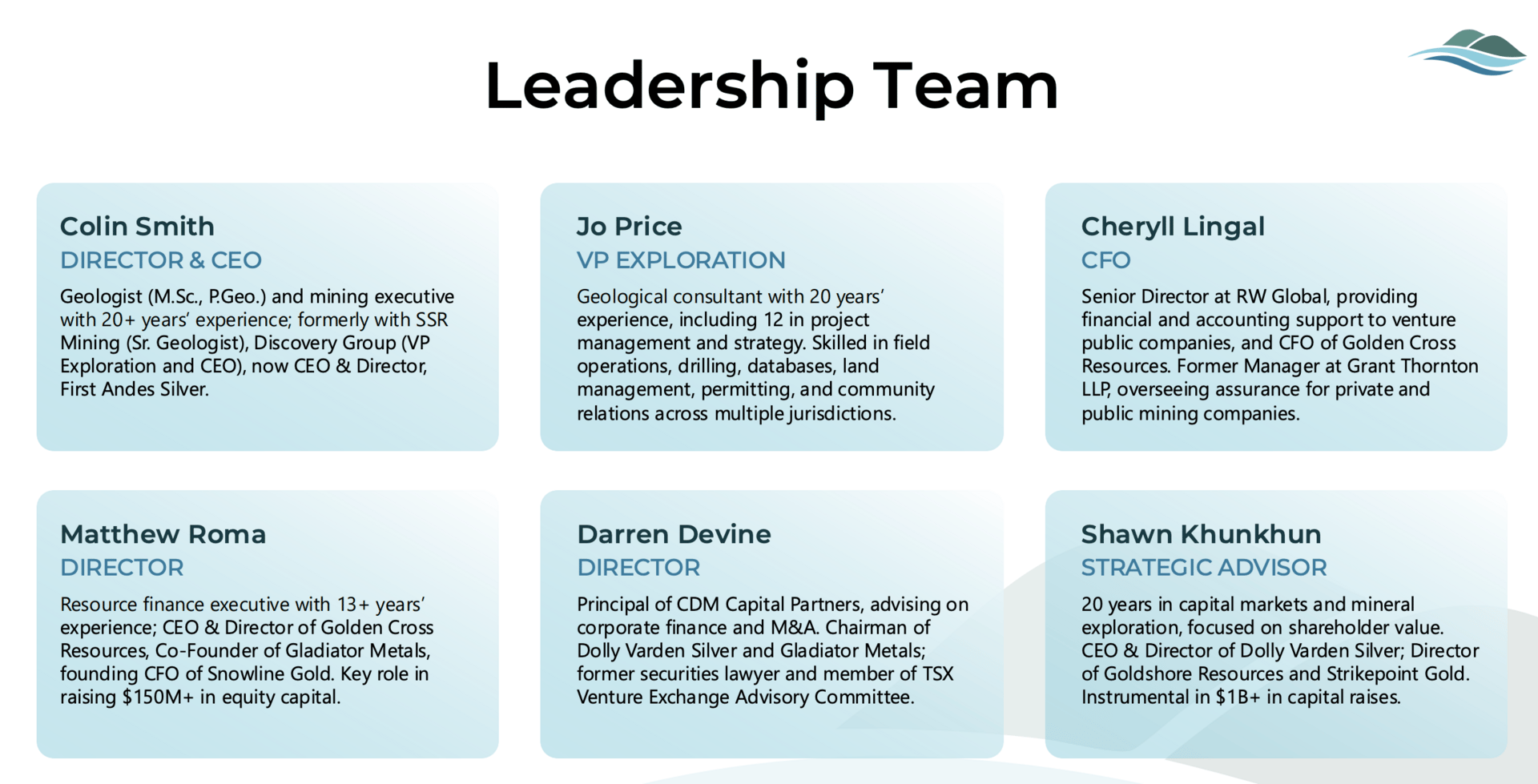

I am excited to see how this team continues to execute, because if its anything like the other companies this team overlaps with, like Matt Roma on Golden Cross and Shaun Khunkhun & Darren Devine on Dolly Varden, which by the way just hit yet another all time high trading of $7.49 $DV.TSXV ( ▼ 2.11% ) and announced a $30M after market bought deal, I don’t think this will be valued in the 10’s of millions for long.

With lots more upcoming catalysts, this should start to get a lot more exciting in the coming weeks and months.

TooGood Gold Corp. (TSX-V:TGC)

Next, a Golden Cross Resources Update (TSX-V:AUX)

I’ve covered Golden Cross for a while now, from $0.38 earlier this year (peaked at $0.95 recently), it’s one of those quiet names that’s suddenly not so quiet anymore.

Random days like yesterday are well over 1M in volume, in fact, they’ve traded over a million shares in each of the last 4 trading sessions, adding up to nearly 9 million total shares.

That volume cannot be ignored because rule #1, usually, in junior mining at least, is volume precedes price.

TSX-V:AUX

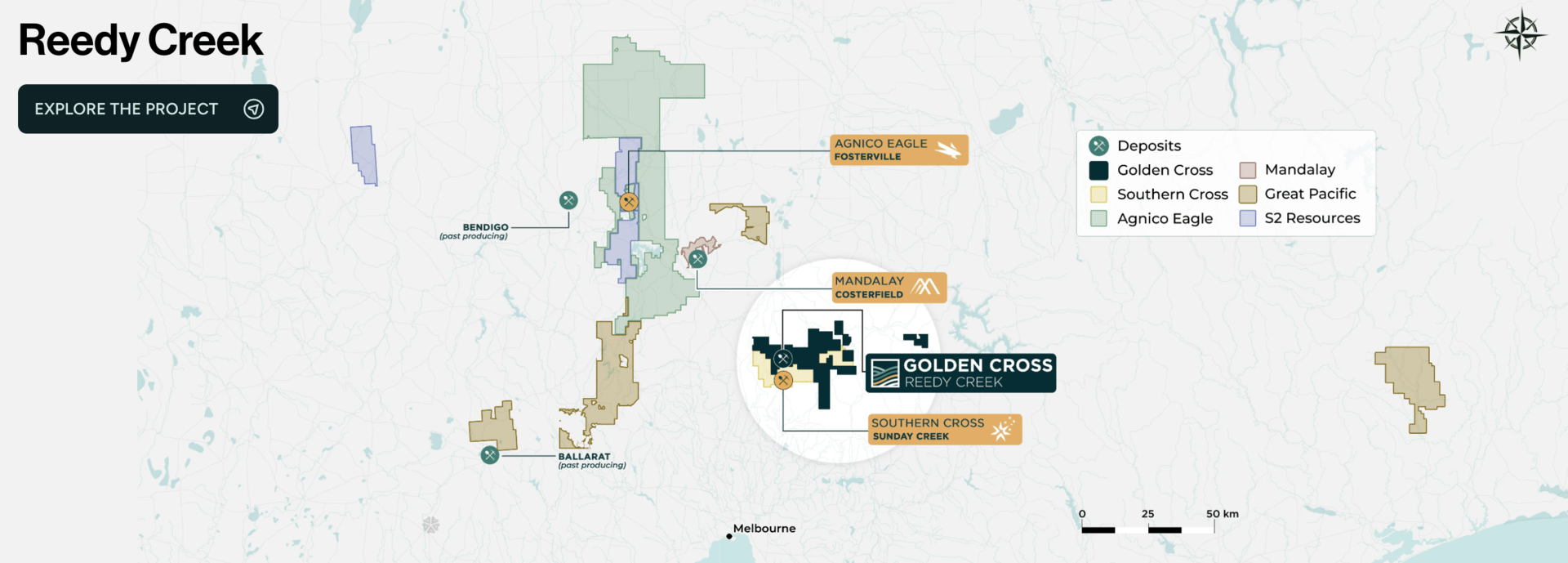

Their Reedy Creek project in Victoria, Australia, has delivered some serious results this far, and has just confirmed what I’ve been waiting to see: high-grade gold with all the hallmarks of a world-class ladder system.

The first assays are in, and they’re strong:

10.8 m @ 2.08 g/t Au from 28 m (incl. 0.5 m @ 24.4 g/t Au)

23 m @ 3.01 g/t Au from 22 m (RWB10)

9 m @ 3.64 g/t Au from 38 m (RWB12)

10 m @ 2.81 g/t Au from 37 m (RWB13)

This isn’t just grade though, it’s geology.

They’re seeing ladder-style laminated quartz veins, arsenic halos, and lots of visible gold.

These are the same geological signatures that underpin Victoria’s most famous mines, Fosterville and Costerfield (both multi-billion).

Fosterville and Costerfield are quite close

I won’t call it a discovery, yet, but these early results indicate structural and geochemical data which gives these guys a roadmap to tap into the richest zones.

That means lower drill risk, lower cost, and higher efficiency.

All three of which are critical to any junior mining exploration program.

They also have 1,900m of further assays pending, that’s a lot more near term catalysts to potentially take the stock higher, or lower for that matter, but given what they’re already intersecting, I think the latter is more unlikely. (I had to word it awkward like that for the pun and to remind everyone it’s actually me writing this)

Anyway, what also has me excited is phase 2 is locked and loaded.

And what’s that you might ask? Well glad you did.

Phase 2 is a fully funded 10,000m drill program with two rigs already turning.

Matt Roma summed it up well: this is shaping up to be a classic Victorian-style gold system, and the deeper they go, the better it could get.

Golden Cross is early in the story, but with Fosterville-style signals showing up in their core, this one has all the makings of something big.

Golden Cross’s X

Gladiator Metals (TSX-V:GLAD)

Gladiator keeps proving out why I called them the Yukon’s next District-scale copper play.

I highlighted the recent financing, and they say it nicely in the most recent PR: “With the recent closing of a $22.5m financing plus existing treasury of $8m, Gladiator is fully funded for significant exploration until the end of 2026."

And I love that.

As such, they’ve just reported assays from first-pass drilling at the Valerie and Little Chief prospects, and the results are opening up entirely new mineralized trends.

Highlights include:

15.8 m @ 0.85% Cu at Valerie in chalcopyrite-veined intrusive with porphyry characteristics

1 m @ 13.35 g/t Au and 1 m @ 7.64 g/t Au to the west of Little Chief Pit — newly identified intrusive-hosted gold mineralization

Strong chalcopyrite + bornite mineralization intersected east of the historic Little Chief Mine (assays pending)

This matters a lot, because Gladiator is now identifying multiple, previously unknown copper-gold skarn and intrusive-related mineralized trends, the type of systems that can scale fast.

On top of Cowley Park (already delivering near-surface, high-grade copper intercepts), they’re rapidly proving that the 35 km Whitehorse Copper Belt could be a true district-scale porphyry and skarn system.

And they’re not slowing down:

A fourth drill rig has now been mobilized to accelerate drilling at Valerie and Little Chief.

IP geophysical surveys are underway to refine targeting.

And with the recently closed $22.5M financing plus $8M already in the treasury, Gladiator is fully funded, as mentioned, for the aggressive exploration plan through 2026.

Jason Bontempo (CEO) put it best: Gladiator’s first drilling of new gravity targets has already intersected multiple new mineralization styles, potentially indicative of a copper-porphyry system, across a 12 km corridor.

That is powerful, and that’s why they’re attracting so much capital.

This could be huge, and I’ll be so bold as to say this: Gladiator isn’t just drilling one deposit. They appear to be unlocking an entire belt.

Time will tell.

Lastly, Mineros S.A. (TSX:MSA)

Ahhh, Mineros, my favorite South American gold producer.

First covered at $2.40, this is the little engine that keeps on chugging, improving, and impressing.

From $2.40 to $4.69

A steady gold producer with real cash flow, a rarity in today’s junior space.

I’ve already covered their record Q2 numbers, but I want to highlight a couple points before going into their share buy-back.

Revenues hit a record $182.4M in Q2 (and $343M in H1).

Net profit also a record at $43.5M in Q2 ($81.5M in H1).

EPS came in at $0.15 for the quarter ($0.27 for H1).

Operating cash flow topped $59.8M in Q2 and $71.5M for H1.

Cash on hand: a very strong $109.7M.

Production was solid with 53,907 oz Au in Q2 (33k from Nicaragua, 21k from Colombia).

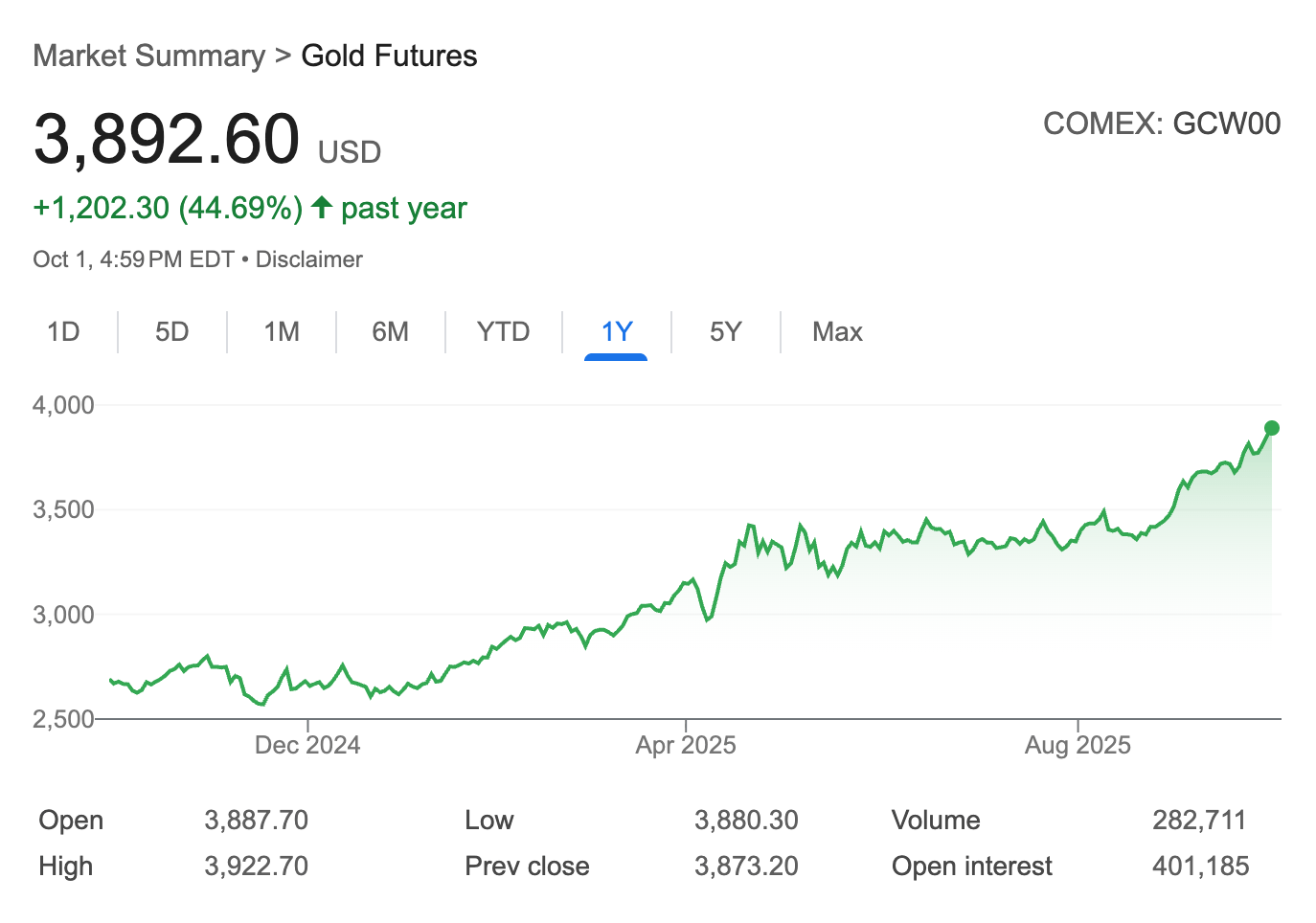

Costs came in at $1,671/oz cash cost and $1,940/oz AISC — still very competitive given the realized gold price of $3,313/oz in Q2.

Their CEO David Londoño highlighted that record gold prices (+42% year-over-year) turbocharged (fantastic word) their profitability, and the balance sheet now gives them the flexibility to pursue both organic growth (like the Porvenir Project at Hemco) and M&A opportunities.

This is exactly what I’ve been talking about for months on X.

When gold moves up, the profitability of producers isn’t linear, its exponential, it’s turbocharged.

Which is why, I can imagine, they’re starting to make moves like buying back their own stock.

They just bought back $12M, purchasing 3.95M shares.

That reduced the float from 299.7M to 295.8M shares, directly increasing shareholder value, and part of the reason the stock cranked from $3.40 to $4.20 in early Sept.

And yes, the dividend machine keeps rolling, with another $7.5M paid out in Q2.

On the operations side, they’re ramping up their brand-new Aurora Plant at Nechí in Colombia.

Built for $6.5M, this floating recovery system will soon process 10,000Tpd using GPS-guided precision and zero chemicals.

As their CEO Londoño puts it: “We continue to see significant upside and believe Mineros’s current share price offers real value compared to peers. With over $109M in cash, a strong balance sheet, and projects like Aurora coming online, we are committed to maximizing stakeholder value.”

The Bottom Line:

Record revenue & profit in Q2

Accretive buyback & dividends

New low-cost plants ramping for higher production and recoveries

Strong balance sheet with serious firepower for growth

Growing resource base with recent acquisitions

Mineros gives you the rare combo of dividends AND growth, while the price of gold keeps getting better and better.

Gold baby Gold

Key Take-Away

TooGood Gold is making a discovery in Newfoundland.

Golden Cross is proving up a ladder system in Victoria.

Gladiator is proving up a district in the Yukon.

And Mineros is generating hand over fist cash flow, while securing the future.

Four very different names, but all delivering real catalysts right now.

The market is starting to wake up… are you?

As always, Happy Hunting!

About The Net Worth Club

Welcome to The Net Worth Club — a no-fluff, high-conviction investing newsletter written for people who want to grow their wealth intelligently and aggressively.

Every week, I break down actionable opportunities across the stock market, private deals, and the global economy — all with one goal in mind: help you multiply your net worth.

You’ll get:

✅ Deep dives on overlooked companies with potential to double (or more)

✅ Real-time trade ideas and portfolio updates — I eat my own cooking

✅ Market psychology, timing strategies, and hard-earned lessons

✅ A front-row seat to how I’m building serious wealth — and helping others do the same

This isn’t financial fluff or recycled headlines. It’s boots-on-the-ground insight, from someone who's in the trenches — raising capital, taking companies public, and making real bets with real money.

If you’ve ever thought: "I just want someone sharp to help me spot the big moves early" — this is for you.

👇 Subscribe now and start compounding smarter:

Read more previous stock picks:

$TSLA ( ▲ 8.46% ) at $180 before moving to $480

$SOFI ( ▲ 1.73% ) at $6.00 before moving to $22.00

$INVZ ( ▲ 14.35% ) at $0.74 before moving to $3.00

Disclaimer: The Net Worth Club shares background information and insights on early-stage companies using publicly available sources. We do not provide investment advice, we are not financial advisors, and nothing we write should be interpreted as a recommendation to buy or sell securities. Our content is intended solely for informational and educational purposes. The information we present may not be complete, accurate, or up to date. If you're interested in a company mentioned in this newsletter, we strongly encourage you to do your own research and consult directly with the company or your licensed investment advisor. From time to time, The Net Worth Club may be compensated by companies featured in this newsletter for awareness campaigns. This creates a conflict of interest and impacts our objectivity. Additionally, the principals of The Net Worth Club may hold, buy, or sell shares of mentioned companies at any time without notice. We are not registered or licensed by any securities regulatory authority in any jurisdiction. Always do your own due diligence and speak with a licensed financial professional before making any investment decisions. Investing carries risk. Never invest money you can't afford to lose. This newsletter is not a solicitation or offer to buy or sell any securities, nor is it a guarantee of performance. Any references to past or potential performance are not indicative of future results.