- The Net Worth Club

- Posts

- This Under $0.20 Gold Stock Is Building a Mine Right Now—and Hardly Anyone’s Watching

This Under $0.20 Gold Stock Is Building a Mine Right Now—and Hardly Anyone’s Watching

The Fully Permitted, Under-the-Radar Gold Developer You’ve Never Heard Of

Danny Brody

May 14, 2025

Gold just broke $3,400 an ounce.

Scrooge McDuck Diving into Gold, 2025

It didn’t grind. It ripped through it.

Now, the smartest people in the sector, many with decades of experience, are calling for $4,000, $5,000, even $6,000 gold.

Some are going further, talking about $10,000, $15,000, even $25,000 per ounce.

Why?

Well, to quote a dear friend (not actually a friend) Ray Dalio in How I Learned to Anticipate the Future by Studying the Past — the clues are always there if you’re paying attention.

And history’s loudest clue came in the 1970s.

Back in the 1970s, gold went on a historic run — rising over 20x in a single decade after Nixon pulled the U.S. off the gold standard.

From just $35/oz in 1970 to a peak of $850 by 1980, the metal became the ultimate hedge against inflation, geopolitical chaos, and broken trust in fiat currency.

Sound familiar?

Today, with global debt spiralling, central banks hoarding gold, global tariff tension, wars, and monetary policy hanging by a thread, serious investors are forecasting a similar setup not for $4,000 or $5,000 gold, but $10,000, $15,000, even $25,000 per ounce.

If history rhymes, we’re not late… we’re early.

But they’re not buying bullion.

They’re buying equities.

The right ones.

The small-caps that are about to become producers. That’s where the leverage lives.

This isn’t just a trade, either — it’s a setup.

We’re not chasing charts…

We’re not jumping on some overbought senior that moves 2% when gold’s up 10%…

We’re early.

With a company that’s:

Fully permitted

Funding commitments in place

Advancing toward construction

And still trading for pennies.

Yet, nobody’s watching…

But that’s about to change…

A Simple Gold Thesis

Gold is doing what gold does when the world gets a little weird: it’s breaking out.

And breaking out majorly.

Geopolitical risks. Rising debt. Declining trust in global institutions. Central banks are repositioning fast—and they’re doing it with gold.

The smart retail investors?

The ones reading this right now? (😉)

They’re following suit.

But while most are reaching for ETFs or physical metal, the real upside is elsewhere.

It’s in the equities.

But not just any equities.

You want the sweet spot!

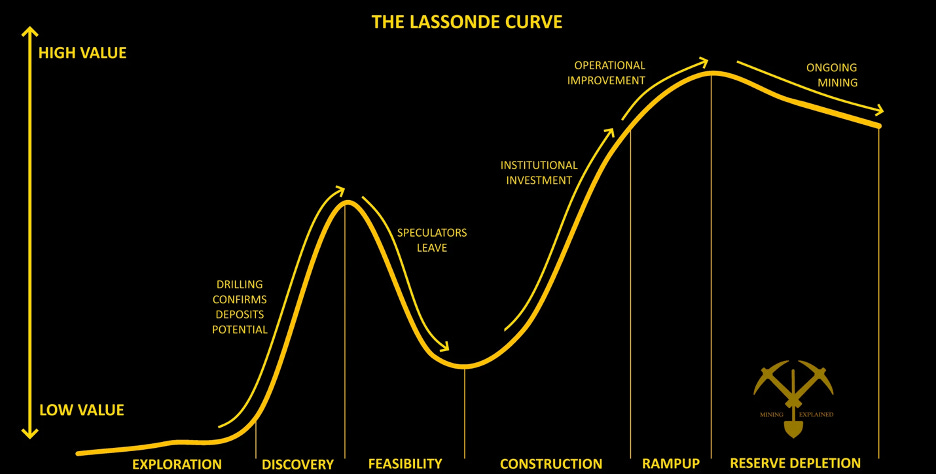

The Sweet Spot: When a Junior Becomes a Producer to Fund Exploration and Avoid Dilution

The big re-rates in gold equities don’t come when you go from explorer to explorer with more drills. (Well, they do sometimes, but it’s always short lived.)

They come when you build. When you cross that chasm and show the market this isn’t a science project anymore.

They come right in between Feasibility and Construction.

That’s when the institutional money steps in. That’s when majors take notice.

And that’s when serious shareholders start seeing real returns.

And I think I’ve found one of those such companies…

Here’s where it gets exciting.

They could be less than 12 months from production.

They’re backed by the biggest names in the country they operate in.

They’re sitting beside a Tier 1 mine owned by one of the world’s largest producers.

They have permits, people, partners — and no cheap paper.

They just haven’t told their story…

Until now.

The Anatomy of a Breakout

So what does this setup look like?

Let’s walk through it.

1. They Have a Fully Permitted, Construction-Stage Gold Mine

This company didn’t just stake some claims and start tweeting.

They acquired a project with two JORC compliant pre-feasibility studies, built a 300,000-liter water tank, placed a deposit on the ball mill, and started site prep.

They’re aiming to pour gold from their ~300,000 oz historical resource estimated deposit by May 2026.

And they have a 10-year mining license already granted.

No permitting risk.

No guessing games.

This isn’t a hope-and-dream operation. It’s happening.

2. They Brought In the Biggest Local Partner Possible

The project is being developed with support from one of the country’s most influential mining contractors — a billionaire whose company provides mining services to majors like Barrick, AngloGold, and De Beers.

This isn’t just investment.

It’s political alignment, construction firepower, and operational track record — all rolled into one.

3. The World’s Second-Largest Gold Miner Is Already a Shareholder

This major doesn’t dabble. When they get involved, it’s for a reason.

They bought in at $0.27. The stock trades well below that.

And guess what?

They’re also drilling next door. Literally.

We’ll say that again: The biggest company in the region is operating right next door, with a 12.6M oz deposit. (Proven, measured & indicated, and inferred)

And this company still holds upside exposure to discoveries made on ground they sold to that major.

It’s a multi-path upside scenario that’s incredibly rare.

4. They Kept Their Share Structure Tight

No warrants.

A proper share structure.

80% owned by insiders and strong hands.

It’s exactly the kind of cap table I look for.

Management built the cap table for one purpose: to benefit execution — not hype.

That’s rare.

And when the re-rate begins, it’s going to matter.

5. They Have a Second Asset That Could Be the Real Prize

If the flagship mine is the production story, this second project is the exploration wildcard.

It sits right beside one of Africa’s largest gold deposits.

It’s already been drilled—over 50,000 meters—with multiple hits in the 20 to 70 g/t range.

It’s not moose pasture. It’s high-grade, high-conviction, high-upside geology.

And I’ve actually been there.

In 2010, I did a site visit, no joke. But it’s only grown since then.

Most juniors would build their entire story around this.

For this company, it’s the bonus.

The game plan, to fund further exploration with cashflow from the mine, is genius.

Why?

Dilution!

This company won’t need to dilute it’s share capital much beyond getting the mine into production.

Meaning, it can use it’s free cash flow from operations to fund it’s entire exploration program.

Do you have any idea how rare that is for a junior?

The Country That Could Be Africa’s Gold Epicenter

For years, Mid to North West Africa was the place to be. Ghana, Mali, Burkina Faso, Côte d’Ivoire.

But coups, instability, and ESG headaches have forced the big players to rethink.

The capital is shifting. And smart money is turning South and East.

Tanzania is quickly becoming the gold center of gravity on the continent.

Over 60 years of stable democracy

English common law

Pro-mining policies

$4B+ invested by Barrick alone

Barrick paying the most tax out of anyone in the country

It’s elephant country… But, under explored.

The same greenstone belts that made West Africa rich run through Tanzania — but have barely been touched.

And this company’s projects are right in the heart of it.

And they’re not the only ones.

Barrick has designated Tanzania as home to its flagship “Tier 1” assets.

Its Bulyanhulu and North Mara mines are two of the highest-grade gold producers in the region.

In 2023 alone, Barrick invested over $600 million in Tanzania.

Perseus has just committed $523 million to develop the Nyanzaga Gold Project in Tanzania.

AngloGold Ashanti is expanding its footprint in the country, and already runs the Geita mine, which is the largest producer in Tanzania by ounces.

So are smaller producers like Shanta Gold and TRX Gold.

And TRX Gold proved it’s possible.

20 kilometers south, they showed it’s possible to go from junior to producer right here.

Its Buckreef project is now pouring gold.

The stock re-rated as it hit key milestones — without needing to exit the country or change jurisdictions.

Investors took notice.

They Didn’t Just Line Up Permits—They Locked In the Money

One of the biggest risks for juniors is how they raise capital.

Too many flood the market with discounted paper and warrants.

This company went a different way.

They secured commitments of up-to $11.5M from their billionaire mining contractor in milestone-based tranches — alignment at its finest.

They’ve signed a term sheet for a bullion-backed loan of 7,000 ounces with a gold lender — structured to avoid fiat currency and equity dilution, with repayment proposed in physical gold.

Between those two moves and funding commitments, they’re essentially funded for the entire build.

And the dilution risk? Practically zero.

The Dream Team

Management matters. Especially when the goal is execution, not just promotion.

Here’s who’s running the show:

CEO – 25+ years in capital markets. Built and backed multiple public companies.

Executive Chairman – Ex-Merrill, ex-BMO, ex-trader. Deep institutional ties. Largest individual shareholder.

COO – Developed this exact mine under its prior owner. Now back to finish it.

Managing Director (Tanzania) – 22 years in-country. Former Barrick exec at the adjacent mine.

Senior Advisor – Built K92 Mining into a $3B juggernaut. $700M+ raised. Dozens of mines built.

This isn’t their first project. It’s not even their tenth.

They’ve been here before. And they’re back because they see what’s coming.

The best part?

The Quiet Phase Is Over

These guys stayed quiet on purpose.

They didn’t run the promo machine while chasing permits. They didn’t pump while looking for funding.

They established the foundation.

They focused on getting the right things in the right places.

And now they’re ready to build. Literally.

This is the moment before the moment.

Construction has begun.

The first pour is in sight.

Drilling on the blue-sky asset is about to start.

All while gold is screaming to new highs.

I hope you’re watching…

Why I’m Watching This One Closely

I’ve been early before.

On trades that turned into multi-baggers. On ideas that the street missed.

This one has the feel.

It’s smaller, but checks the right boxes:

Real asset with near-term cash flow ✅

Strategic neighbors and insider buy-in ✅

Undervalued vs. comps and internal milestones ✅

Capital structure that rewards execution ✅

And exploration torque most juniors only dream of ✅

It’s not often you find a company building a mine with this kind of setup… trading below $0.20.

And it’s almost never when Barrick is on the cap table… (read: takeover?) and the richest man in Tanzania? He’s swinging the excavators, is a major shareholder and financier of the company.

I’m not saying it’s guaranteed.

Nothing is.

But I am saying it’s asymmetric.

If they pour gold next year, as planned? It re-rates.

If the exploration hits next door to a Tier 1 mine? It explodes.

If either of those happens in a +$3,000 gold environment?

Good luck finding liquidity on the ask.

The real setups are the ones that feel obvious… after they’ve moved.

This one doesn’t feel obvious, yet.

Which is exactly why I’m sharing it, now.

🔒 Want the name of this highly undervalued and ready to rip stock?

It’s revealed to free subscribers of The Net Worth Club below: